🔥HOT U.S. MARKETS 🏡 MORE CHOICES FOR BUYERS- JD's Market Pulse

For the week of September 12, 2022

For the week of September 12, 2022

HOUSING AFFORDABILITY? HOTTEST US MARKETS

CLARK COUNTY, NV: SALES DOWN, INVENTORY UP

“The adventure of life is to learn. The purpose of life is to grow. The nature of life is to change.” - William Arthur Ward (American writer)

National Market Update

Hottest Housing Markets: In Search of Affordability

Manchester-Nashua, NH takes the top spot on the hottest housing markets list in August, holding the top spot for the tenth time in the last year.

The top 20 hottest markets are spread out across 13 states, with three metros in Indiana.

As prices begin to level off nationwide, affordability remains a key feature of August’s hottest markets with 16 markets below the national median listing price.

There are no Western region markets on this month’s list again, for the third month in a row.

The Milwaukee, WI metro area saw the largest increase in its Hotness ranking among larger metros compared to last year, climbing 128 spots to rank as the 40th hottest US market in August.

Purchases of new homes slipped to their slowest pace since January 2016. New single-family home sales declined 12.6% to 511,000 units in July from a pace of 585,000 units in June and were down 29.6% year-over-year.

The inventory of homes for sale rose. The listed inventory of new homes for sale, at 464,000 units for the end of July, increased 3.1% m/m and 28.2% y/y. That inventory would support 10.8 months of sales at the current sales pace, up from 9.2 months in June.

Forbearance on mortgage loans continued to decline. The MBA Forbearance Survey shows the share of homeowners with mortgages in forbearance was 0.74 percent (370,000 households) in July, down from 3.40 percent one year ago. The forbearance rate was only 0.25 percent of all home loans in the beginning of March 2020, before the economic effects of the COVID pandemic began to be felt.

The U.S. homeownership rate rose in the second quarter. The national homeownership rate increased to 65.8 percent in the second quarter of 2022 from 65.4 percent in the first quarter. Caution should be used in comparing this rate to the 2021 second-quarter estimate because COVID-19 prevented normal data collection procedures during that time. The historic norm since 1965 is 65.2 percent. (Source: Census Bureau)

Economic Notes

During a light week for economic data, investors were focused on U.S. and European central bankers. There were no surprises from the European Central Bank (ECB) or U.S. Fed Chair Powell, however, and mortgage rates ended the week with little change.

With inflation surging to decade highs, the ECB raised interest rates by a massive 75 basis points to the highest levels since 2011. The latest readings showed inflation in the eurozone at an annual rate above 9%, far above the target level of the ECB of 2%. ECB chief Lagarde explained that the increase in rates was necessary because inflation is likely to stay above the target for "an extended period." Investors expect additional 50 basis point rate hikes at the next two meetings.

On Thursday, Fed Chair Powell repeated that he is "strongly committed" to fighting inflation. He emphasized the importance of reducing inflation before the public starts to view higher levels as normal and makes future plans based on it. According to Powell, Fed officials hope that higher rates will bring the strong labor market back into "better balance" to reduce outsized wage increases and lessen inflationary pressures. Investors anticipate a 75 basis point rate hike at the next meeting on September 21.

The most significant economic report released this week from the Institute of Supply Management (ISM) provided additional evidence that consumers are shifting their spending from goods to services. The national services sector index rose to 56.9, which was stronger than expected. Levels above 50 indicate that the sector is expanding.

Going forward, investors are hoping for more specific Fed guidance on the pace of future rate hikes and bond portfolio reduction. The Consumer Price Index (CPI) will be released on Tuesday. CPI is a widely followed monthly inflation indicator that looks at the price changes for a broad range of goods and services. Retail Sales will be released on Thursday. Since consumer spending accounts for over two-thirds of U.S. economic activity, the retail sales data is a key measure of the health of the economy. Import Prices also will come out on Thursday.

Calendar

- Tue. 9/13 CPI

- Wed. 9/14 PPI

- Thu. 9/15 Retail Sales

- Thu. 9/15 Import Prices

Inverted Yield Curve Watch

30 Year Treasury Yield: 3.524%

10 Year Treasury Yield: 3.375%

5 Year Treasury Yield: 3.47%

2 Year Treasury Yield: 3.582%

Local Market Update (Southern Nevada)

Clark County, NV Absorption Rate

21.01%

The current absorption rate for the Southern Nevada market the past four weeks is 21.01%, down 0.78% from last week's absorption rate. This marks the first decrease in the absorption rate after last weeks increase, which saw ten consecutive weeks of a decline prior to the September 5, 2022 market update.

A market with an absorption rate at or above 20% is typically called a seller’s market, whereas an absorption rate below 15% signals a buyer’s market.

Each week we will update the current median price for the current month. Keep in mind the majority of sales occur at the end of the month, so official numbers will be published on the first Monday of each month.

Current September Median Prices

Single Family

$450,000

(Unchanged from August of $450,000)

Condo

$225,500

(Down from August of $232,000)

Townhouse

$314,500

(Down from August of $325,000

)

The past 26 weeks have seen an increase of residential resale inventory available on the open market in Southern Nevada. This week however shows an increase of only 7 more residential resale properties on the market compared to one week ago, a sign that inventory may be peaking. The previous week saw an increase of only 18 properties on the resale market, further confirmation that the inventory is beginning to peak. Chart below shows total available inventory to total weekly closed sales. (Last updated September 12, 2022)

As of September 12, 2022, there are currently active (%’s versus 4 weeks ago):

8,465 Single Family Homes +3.04%

1,139 Condos +4.98%

777 Townhouses +5.57%

317 Manufactured Homes +16.12%

435 High Rise Units -1.58%

94 Multiple Dwellings -5.05%

2,618 Parcels of Land +5.01%

3,111 Rentals On Market +5.64%

Past Seven Days Market Watch (%’s versus 4 weeks ago):

1,027 New Listings -15.82%

205 Back On Market -13.50%

78 Price Increases -19.59%

1,789 Price Decreases -5.99%

625 Accepted an Offer -26.81%

481 Sold -11.90%

87 Expired +1.16%

473 Taken Off Market -11.90%

86* properties are coming soon +/- 0.00%

This week, there are 7 more active residential resale properties on the market compared to one week ago for a total of 11,127, an increase of 0.06%.

*Properties coming soon do not indicate all of the upcoming properties. These are listing that are entered into the MLS prior to list date.

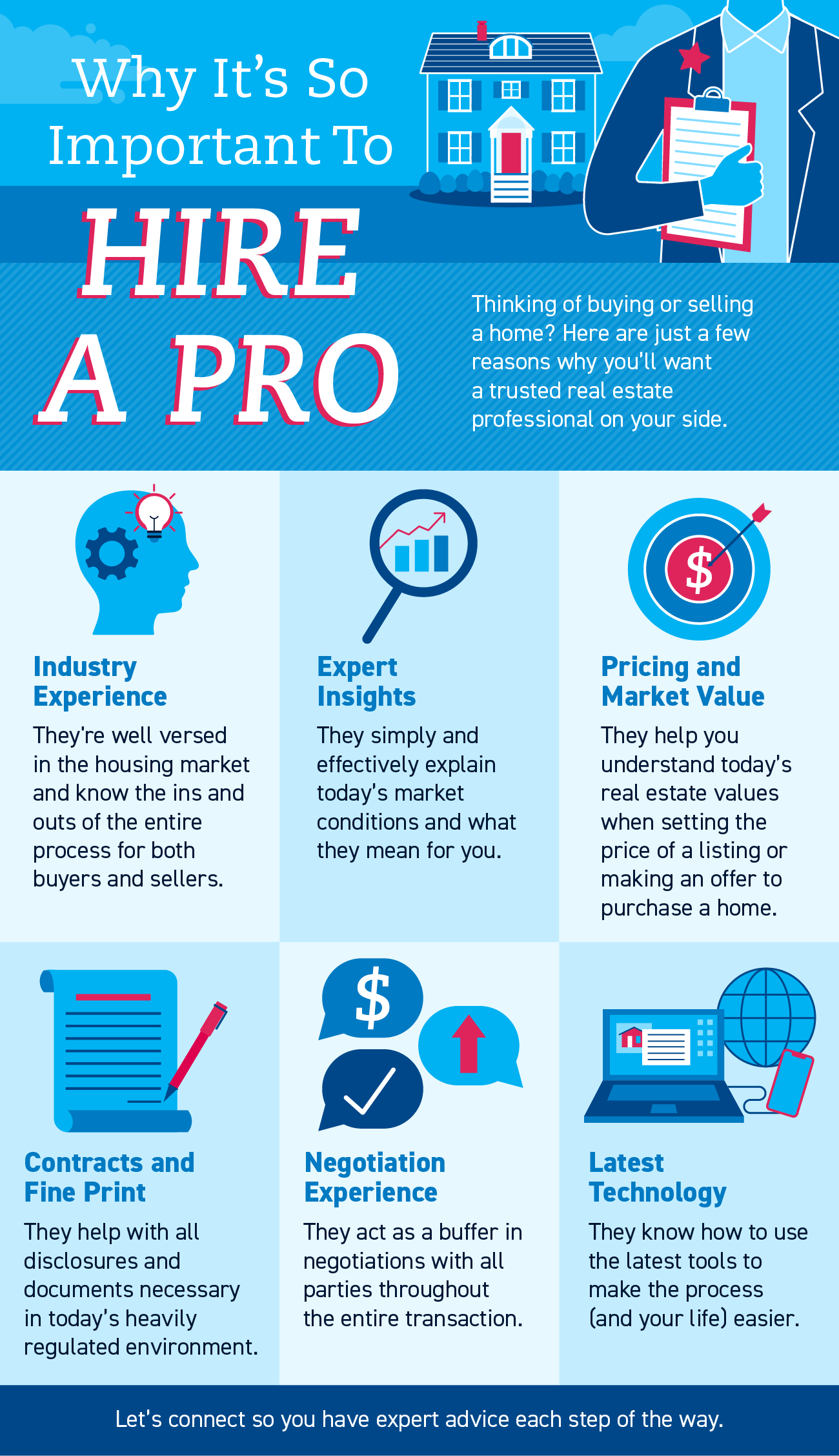

If you’re thinking of buying or selling a home, you’ll want a trusted real estate professional on your side for their industry experience and expert insights.

The right advisor utilizes the latest technology and can help you navigate today’s home pricing and market values, the contracts and fine print, and the negotiations you’ll face.

Let’s connect so you have expert advice each step of the way.

FEDERAL RESERVE WATCH

Forecasting Federal Reserve policy changes in coming months. The Fed Funds Futures market expects rate hikes for the rest of the year, starting with a three-quarter percent bump this month. Note: In the lower chart a 84.0% probability of change is a 84.0% probability the rate will rise. Current rate is 2.25%-2.50%

AFTER FOMC MEETING ON: CONSENSUS

Sep 21 3.00%-3.25%

Nov 2 3.25%-3.50%

Dec 14 3.50%-3.75%

Probability of change from current policy:

AFTER FOMC MEETING ON: CONSENSUS

Sep 21 84.0%

Nov 2 92.5%

Dec 14 90.4%